So if you have $3,000 owed to you by Mr. Smith, you have a debtor, an asset, worth $3,000. In accounting we have specific criteria which need to be fulfilled in order to recognize an asset in our accounting records. Now that you know how assets are acquired, let’s look at how they are classified. This article how to read your practice’s accounts receivable aging report and related content is the property of The Sage Group plc or its contractors or its licensors (“Sage”). Please do not copy, reproduce, modify, distribute or disburse without express consent from Sage. This article and related content is provided as a general guidance for informational purposes only.

Intangible Assets – These are a class of assets that aren’t going to have any kind of physical presence. Intangible assets will get accounted for differently depending on the specific type. Assets can be wide-ranging and get used in a handful of ways; for example, they can generate cash flow, improve sales, or reduce expenses. Assets need to be controlled by whoever owns them, giving owners certain legal rights and to be able to use the asset accordingly. When conducting diligence on a company to arrive at an implied valuation, it is standard to evaluate just the performance of operating assets to isolate the company’s core operations. The assets are ordered on the basis of how quickly they can be liquidated, so “Cash & Equivalents” is the first line item listed on the current assets section.

Comparison: current assets, liquid assets and absolute liquid assets

This group includes land, buildings, machinery, furniture, tools, IT equipment (e.g., laptops), and certain wasting resources (e.g., timberland and minerals). They are written off against profits over their anticipated life by charging depreciation expenses (with exception of land assets). Accumulated depreciation is shown in the face of the balance sheet or in the notes. It’s also important to note that the different types of assets in accounting are expensed in different ways. Although both processes describe similar things, depreciation is used for tangible assets (assets with a physical presence), whereas amortization is used for intangible assets.

The more frequently you update your balance sheet, the more accurate your accounting books will be. It’s important to recognize that an asset must be owned and controlled to have certain legal rights, and needs to have some sort of value. This means that whoever owns the asset will receive some type of future benefit. But if the asset has no physical form and cannot be touched, it is considered to be an “intangible” asset (e.g. patents, branding, copyrights, customer lists). Since only one month would have passed by 31 December out of the three-month period covered by the advance, two months’ rent will be recognized as a prepaid asset in the balance sheet. Lou paid a 3-month advance amounting to $3000 for a small painting studio that she rented on 1 December 2020.

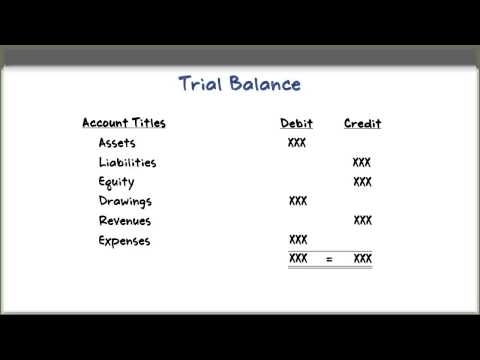

Assets

The balances in the asset accounts will be summarized and reported on the company’s balance sheet. Creditors and investors keep a close eye on the Current Assets account to assess whether a business is capable of paying its obligations. Many use a variety of liquidity ratios, representing a class of financial metrics used to determine a debtor’s ability to pay off current debt obligations without raising additional funds. This account may or may not be lumped together with the above account, Current Debt.

Unlike assets and liabilities, expenses are related to revenue, and both are listed on a company’s income statement. Publicly-owned companies must adhere to generally accepted accounting principles and reporting procedures. Following these principles and practices, financial statements must be generated with specific line items that create transparency for interested parties. One of these statements is the balance sheet, which lists a company’s assets, liabilities, and shareholders’ equity.

Asset Recognition Criteria in Accounting

The non-current assets section includes the long-term investments of the company, whose potential benefits will not be realized in a single year. Some assets provide direct economic benefits (e.g., inventory), whereas others indirectly contribute to the future cash flows of a business (e.g., office computer). When looking at an asset definition, you’ll typically find that it is something that provides a current, future, or potential economic benefit for an individual or company. An asset is, therefore, something that is owned by you or something that is owed to you. A $10 bill, a desktop computer, a chair, and a car are all assets.

Here are some examples of assets and their future economic benefits. AT&T clearly defines its bank debt that is maturing in less than one year under current liabilities. For a company this size, this is often used as operating capital for day-to-day operations rather than funding larger items, which would be better suited using long-term debt.

- An asset is, therefore, something that is owned by you or something that is owed to you.

- So far, I have explained what assets are, their characteristics, and types, but as an accounting beginner, it’s equally important for you to learn about what are not assets.

- As companies recover accounts receivables, this account decreases, and cash increases by the same amount.

- Property, plants, buildings, facilities, equipment, and other illiquid investments are all examples of non-current assets because they can take a significant amount of time to sell.

- Marketable Securities is the account where the total value of liquid investments that can be quickly converted to cash without reducing their market value is entered.

AP can include services, raw materials, office supplies, or any other categories of products and services where no promissory note is issued. Since most companies do not pay for goods and services as they are acquired, AP is equivalent to a stack of bills waiting to be paid. For example, if a company has had more expenses than revenues for the past three years, it may signal weak financial stability because it has been losing money for those years. Generally, liability refers to the state of being responsible for something, and this term can refer to any money or service owed to another party.

This is the asset’s estimated value if it was broken down and sold in parts. In some cases, the asset may become obsolete and will, therefore, be disposed of without receiving any payment in return. Either way, the fixed asset is written off the balance sheet as it is no longer in use by the company. It’s going to depend on the type of business you operate and where you’re located in the United States. Generally, businesses can create assets by purchasing land, buildings, machinery, and equipment.

Physical Existence Classification

Some examples of fixed assets include cars, land, buildings, and machinery. Current assets are items of value your business plans to use or convert to cash within one year. Most businesses use current assets in their day-to-day business operations. Current assets are also considered short-term investments because you can convert or use them within one year.

Australian lawmakers reject Andrew Bragg’s crypto bill – Cointelegraph

Australian lawmakers reject Andrew Bragg’s crypto bill.

Posted: Mon, 04 Sep 2023 16:30:00 GMT [source]

Many businesses have loans, notes, and leases on equipment that either directly or indirectly eliminates their true ownership of the resources, but they still have control of it. Because current assets are more liquid, list them higher up on your balance sheet. Fixed assets are less liquid, meaning you list them further down on your balance sheet. Fixed assets are particularly important to capital-intensive industries, such as manufacturing, which require large investments in PP&E. When a business is reporting persistently negative net cash flows for the purchase of fixed assets, this could be a strong indicator that the firm is in growth or investment mode.

Being fixed means they can’t be consumed or converted into cash within a year. As such, they are subject to depreciation and are considered illiquid. Prepaid expenses—which represent advance payments made by a company for goods and services to be received in the future—are considered current assets. Although they cannot be converted into cash, they are payments already made. Prepaid expenses might include payments to insurance companies or contractors. Current Assets – Current assets can get converted into cash within 1 year.

Tangible assets are subject to periodic depreciation while intangible assets are subject to amortization. The asset’s value decreases along with its depreciation amount on the company’s balance sheet. The corporation can then match the asset’s cost with its long-term value.

Asset accounts are referred to as permanent or real accounts since they are not closed at the end of the accounting year. Instead, each asset account’s balance at the end of the accounting year is carried forward to become the beginning balance of the next accounting year. Two asset accounts, Allowance for Doubtful Accounts and Accumulated Depreciation, are known as contra asset accounts since these accounts are expected to have credit balances. Companies of all sizes finance part of their ongoing long-term operations by issuing bonds that are essentially loans from each party that purchases the bonds.

I talk about how each should be accounted for with examples and explanations in each article. In our short example, we saw three ways three different assets were acquired. First, the company acquired equipment by a contribution from its owners. Second, the company used its own assets to purchases more assets when it bought additional equipment with its cash. While reporting your assets on your business’s balance sheet, you must record them in descending order, based on their level of liquidity.